Rising Interest Rates Amidst Uncertain Times — Is The Bullish Property Market Coming to an End?

In a similar article that I wrote previously, I shared my sentiments on how rising interest rates and rising property prices will affect investor’s game plan. Do check out my previous article ‘Rising Interest Rates vs. Rising Property Prices — Should I Act Now Or Wait?’ to find out what other opportunities there are that you can consider.

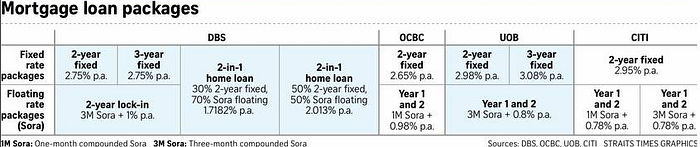

DBS Late to the Party in Raising Home Loan Rates

On the night of 28 June 2022, Singapore’s largest lender DBS Bank joined UOB and OCBC in increasing their home loan rates. They also scraped their 5-year fixed rate package for HDB flats. At its new rate of 2.75% per annum, DBS’ fixed rate packages are now the priciest among the 3 local banks. The US Federal Reserve has raised interest rates aggressively to counter inflation and global leaders tend to follow suit. Unfortunately, there is no relief in sight for home buyers as the Fed has announced that it will continue to hike rates and so will banks in Singapore.

Judging from the pace that Singapore interest rates are increasing, fixed mortgage rates are set to revert back to pre-covid times at around 2.9%. Inflation has never reached such highs over the past decade in the US and in Singapore, and unless the resulting energy crisis from the Ukraine-Russia War is resolved, inflation will continue to pose a problem. On the bright side, I would not expect the Feds to hike interest rates too aggressively for fear of sliding into a recession.

Singapore’s Real Estate Prices at All Time High — What Will Happen to the Next Few Launches?

It is no longer a speculation that property prices will continue increasing. Property prices have been on an uptrend ever since Covid-19. Till date, Piccadilly Grand and Liv@MB has take-up rates of 79.85% and 80.2% respectively. This gives us a strong indication that demand for new launches is at an all-time high. On 29 June, a 4-room HDB at Tiong Bahru View was reported to have been sold for $1.158 mil with a cash-over-valuation of an astonishing $158,000!

With the recent cooling measures and our Government’s commitment to increasing land supply, where do you think Singapore’s property prices will head next? With more supply, it is only natural that prices will come down should demand persist. However, due to the illiquid nature of real estate it will take time before we see the full effect it has on the market. Unlike the stock market, buyers and sellers are not able to react immediately. Hence, the price will always be a lagging indicator. The next few launches should still see high take-up rates on their launch weekend, simply due to the fact that there are not many new projects to consider in today’s market.

Is There Still Room For Growth in Singapore’s Property Price?

To answer this question, we have to understand the concept of affordability. Residential properties serve a fundamental human need of providing shelter. As such, majority of the population are still homeowners, buying for the utility of having a roof over their heads. One of the key data to focus on would be the Median Household Income.

According to the Singapore Department of Statistics, 21.4% of Singapore’s population stays in private properties. With the growing affluence of Singapore’s residents and the increasing supply of Condominiums in the few years to come, it is only natural to expect this percentage to increase.

Factoring in some high-income earners who choose to live in HDB flats, we focus on 30th percentile household income.

Assuming a $15,000 combined household income at the age of 40, the loan affordability amounts to a $2.2 million purchase price — this is the threshold that the top 30% of households can afford. New launches in the Outside Central Region (OCR) are launching past the $2000psf price, considering a $2100psf price in the near future, the top 30% of households will still be able to afford a 1047sqft unit based on a maximum purchase price of $2.2 million.

While it is not entirely accurate to say that the top 30% of households will be able to afford a $2.2 million property comfortable, it helps us understand the affordability of private housing in the current market. The rate at which property prices grows, will depend on how fast income grows. Nonetheless, if you are worried that the property market may ‘crash’, you can be rest assured because Singapore’s property prices are being suppressed for the longest time. Just imagine what would happen if our Government decides to make do without ABSD. Do you think property prices will stay the same?

It is important to note that cooling measures is aimed at controlling the growth of property prices and not stop it so that an asset bubble will never be formed.

Rising Interest Rates — Should I Wait Out This Inflationary Period?

The lowest fixed rate now is 2.65% per annum at the date of writing. UOB has also recently increased its 2-year fixed rate to 2.98% and implemented a new 3-year fixed rate at 3.08% per annum.

Interest rates will continue to rise in the near future but may fluctuate depending on the US Feds. Property prices, on the other hand, will definitely continue an upward trend. What is uncertain is the rate at which property prices increase.

For comparison, I calculated the estimated monthly payment for a 970sqft unit (average size of new 3-Bedroom units) at 2 scenarios.

Scenario 1:

- time period: current

- $2100 psf

Scenario 2:

- time period: future

- $2400 psf

Assuming that in the future, interest rates will drop to 1.8%, higher property prices will result in higher monthly repayments as compared to buying at the high interest rate environment now. Overall, it will still cost you more per month to purchase in the future if interest rates drop.

Conclusion

Currently, what we know is that interest rates are set to increase further. By how much or till when, is the uncertainty. We will also not know when interest rates will decrease. However, if we know that property prices will continue on an upward trend, would it be wise to buy in the future when interest rates drop but prices are higher? I like to think that when investing in properties, it is never about timing the market, but time in the market.

While real estate as an asset class is generally safe in Singapore, there has also been cases where investors suffered losses. Hence, I cannot emphasize enough on the importance of taking calculated risks when investing in real estate. After all, real estate makes up the largest asset for the majority and it is always good to exercise prudence.

I hope this article serves purposeful in helping you make a more well-informed decision, regardless of whether you’re purchasing a property for own-stay or investment. As always, feel free to share your opinion in the comment section and I will take time to address them when I can. Till next time!